Prof. Nouriel Roubini (http://www.rgemonitor.com/blog/roubini) has become so famous recently he could market his own pasta sauce or “credit crunch” croutons? In “How to avoid horrors of ‘stag-flation’” (FT 3, December) he cites a litany of risks and responses that boil down to private sector (banks, businesses and households) running down stocks and de-leveraging with Government and central banks “becoming the lenders of first and only resort”. He quantifies “credit losses”, by which he means pertaining to banks and not also stock market falls and property and business asset losses, “as likely to be close to a staggering $2,000bn.” But, is this in fact “staggering”?

Prof. Nouriel Roubini (http://www.rgemonitor.com/blog/roubini) has become so famous recently he could market his own pasta sauce or “credit crunch” croutons? In “How to avoid horrors of ‘stag-flation’” (FT 3, December) he cites a litany of risks and responses that boil down to private sector (banks, businesses and households) running down stocks and de-leveraging with Government and central banks “becoming the lenders of first and only resort”. He quantifies “credit losses”, by which he means pertaining to banks and not also stock market falls and property and business asset losses, “as likely to be close to a staggering $2,000bn.” But, is this in fact “staggering”?$2 trillions is just over two thirds of the world’s banks’ capital reserves, and twice that of US banks’ ‘own capital’. Yet, this is surely the likely scale to be expected of a relatively severe recession, whether simultaneous globally (rare) or staggered region by region and equates to 3% roughly of banks’ worldwide ‘own assets’. Banks’ gross losses before recoveries will probably be twice this. The action of Governments and central banks is mitigating half of the nominal (short term mark to market) loss, buying time for banks to recover what they can from the mainly paper losses so far (typical recovery over 3 years expected to be worth 55% of impaired debts). Banks have to sell assets, business units and cut costs. Government action combined with banks’ common-sense to preserve their customer-driven business should ensure lending is maintained. Cash wealth becomes more concentrated in recession, but the cash-rich will look to invest for the longer term in discounted assets, especially when deposit rates are low, even in a stagflation environment.

Prof. Nouriel Roubini says “The Fed and the Treasury are taking a massive amount of credit risk, endangering the long term solvency of the US Government.” This strikes me as Roubini hyperbole. The only solvency concern should be short to medium term and that is not at risk when the cash element of US Government support is small and its gross and net Federal Debt is small in ratio to GDP and only one third or smaller than the private sectors of the economy. Government is also financially well placed to gain as much or more than others financially when recovery returns.

Prof. Roubini finishes by saying the worst lies ahead and that the flow of news in 2009 “will be much worse than expected”. Is this not expected? The stock markets have surely discounted the short term ahead already (most stocks over-sold, a third below book value) and Governments, central banks, and even businesses and households generally appear crisis-aware and positioning to manage, or be judiciously helped to do so by Government actions, through the coming slump. For example, just today Gordon Brown is announcing his idea to grant homeowners in financial difficulty the right to demand a two year 'mortgage holiday' guaranteed by taxpayers, in a dramatic bid to prop-up the housing market, which is supported by the UK's 8 largest mortgage lenders! This follows on from similar measures by FDIC and FM&FM in the USA.

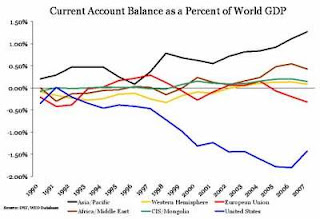

Martin Wolf ("Global imbalances threaten the survival of liberal trade" FT 3 Dec.) has written an excellent and timely tour d'horizen of the global imbalances that led up to the current crisis. His focus now quite rightly on the present more than the recent past, and hence he emphasises the urgent necessity of surplus countries to do more to stimulate endogenous growth. Germany has for years (at least two decades since introducing their unnecessary and economically self-debilitating Einheitssteuer - unification tax - compounded by fiscal policy underpinning the Euro) been extraordinarily resistent to endogenous 'Wachstumsimpuls'. Advisors to the Merkel coalition even in its early days did press for this but where over-ruled. In China and even Japan, there is urgency to support domestic growth impulse. China is trying to enforce its 40 hour week laws (with limited success so far) and has announced a large fiscal boost. There are some structural problems to this in respect of a lack of an established system for inter-regional transfers and relatively weak 'automatic stabilizers'. In Japan, household debt inherited from the late '80s property bubble continues to overhang consumer confidence. The worst case, however, is the EU where the only fiscal boost currently enisaged is worth less than 2% ratio to GDP, notwithstanding that a handful of states will in 2009 breach the 3% budget deficit limit set by the Maastricht Agreement. This is surely a time for dusting off the old Delors Plan that proposed an ECU800bn fiscal boost to accommodate the introduction of the Euro. But this plan was voted down 3 times by UK, Germany and the Netherlands. There remains a kneejerk, if not outright cynical, prejudice against borrowing by the European Commission. Instead, the EU's fiscal response envisaged today is about one tenth of this!

Martin Wolf ("Global imbalances threaten the survival of liberal trade" FT 3 Dec.) has written an excellent and timely tour d'horizen of the global imbalances that led up to the current crisis. His focus now quite rightly on the present more than the recent past, and hence he emphasises the urgent necessity of surplus countries to do more to stimulate endogenous growth. Germany has for years (at least two decades since introducing their unnecessary and economically self-debilitating Einheitssteuer - unification tax - compounded by fiscal policy underpinning the Euro) been extraordinarily resistent to endogenous 'Wachstumsimpuls'. Advisors to the Merkel coalition even in its early days did press for this but where over-ruled. In China and even Japan, there is urgency to support domestic growth impulse. China is trying to enforce its 40 hour week laws (with limited success so far) and has announced a large fiscal boost. There are some structural problems to this in respect of a lack of an established system for inter-regional transfers and relatively weak 'automatic stabilizers'. In Japan, household debt inherited from the late '80s property bubble continues to overhang consumer confidence. The worst case, however, is the EU where the only fiscal boost currently enisaged is worth less than 2% ratio to GDP, notwithstanding that a handful of states will in 2009 breach the 3% budget deficit limit set by the Maastricht Agreement. This is surely a time for dusting off the old Delors Plan that proposed an ECU800bn fiscal boost to accommodate the introduction of the Euro. But this plan was voted down 3 times by UK, Germany and the Netherlands. There remains a kneejerk, if not outright cynical, prejudice against borrowing by the European Commission. Instead, the EU's fiscal response envisaged today is about one tenth of this!Martin, in his summary of global imbalances, neglects a major jigsaw piece, which was the role played by securitizations of net financial assets by banks in deficit countries, packaging AAA bonds for sale to surplus countries, some of which foolishly other deficit country banks bought onto their trading books 'for sale'. With Government support this time such asset securitizations may have to be revived in the short to medium term, especially of surplus countries do not buy enough of the bonds that deficit country governments will be issuing in large quantities in the next few months and years.

It should be noted too, however, that generally speaking the credit boom in many developing countries did benefit poorer countries. While rich trade surplus countries that do not introduce significant domestic growth impulses may be accused of 'beggar-my-neighbour' policy, we should not beggar poor emerging nations.

No comments:

Post a Comment